Analysts gauge strengths and risks of 2023 economy

“Fasten your seatbelts. We have begun our descent.”

With that line, Andrew Bauer, Vice President of the Federal Reserve Bank of Richmond, kicked off the 2023 Economic Outlook in the latest BC&E Construction Blueprint Series webinar.

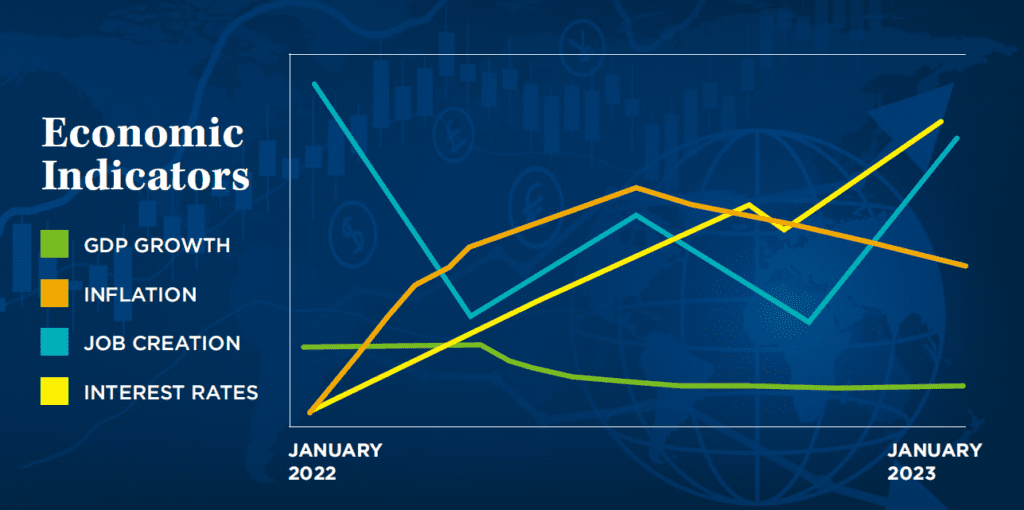

Economy watchers are struggling to predict how the next year will impact American companies, workers and consumers. Many forecasts project the U.S. could slide into a recession this year as the country grapples with lagging GDP numbers and escalating interest rates. At the same time, however, unemployment has hit a 50-year low, inflation has eased slightly and the economy will soon start receiving large infusions of capital from the federal infrastructure package and CHIPS act.

At February’s Construction Blueprint webinar, Bauer and three representatives of MacKenzie Capital —President John Black, Vice President Brendan Harman and Analyst Jack Ward — offered their best analysis and insights. The session was moderated by Annette Walter, CEO and President of Timber Industries.

Recessions, Bauer said, are typically triggered by an unanticipated situation that creates a serious imbalance in one sector of the economy, such as the subprime lending crisis in 2008-09 or the dot-com bust in 2001.

“When you think about 2023 and are we going to have a recession, it is really difficult to see where we have the overextension, where there is a supply-demand imbalance,” he said. “That’s not to say there aren’t a lot of risks in this economy, but this would be the most forecasted and telegraphed recession in U.S. economic history. My expectations are for things to be slow this year but, absent some other external shock, I think we could get through without a recession.”

Bauer pointed to several factors that could produce a slow but solid economy in 2023. Growth in consumer spending, which accounts for two-thirds of the U.S. economy, remained solid in 2022 at nearly 2 percent and, so far, shows no indication of tapering off in 2023. The U.S. labor market grew by 200,000 to 300,000 jobs each month in the second half of 2022 and created more than 500,000 jobs this January.

Monthly new job numbers of 150,000 to 200,000 are considered a benchmark of a good economy so recent job creation “is a strong indication that the economy is still doing quite solidly,” Bauer said.

Not every economic indicator is rosy, however, and the current economy is not an easy or low-risk environment.

The Personal Consumption Expenditure (PCE), an inflation metric, has fallen from its peak of 6.3 percent last September to 5 percent in December. However, that figure is still well above the 2 percent inflation rate that has long been a standard component of a robust U.S. economy. Webinar panelists agreed that the speed with which the United States brings inflation back down to 2 percent will profoundly influence the health of the overall economy.

Meanwhile, interest rates constitute another current difficulty and future risk. The prime rate climbed rapidly and unexpectedly from 2.5 percent a year ago to 7.5 percent currently, and the Federal Reserve Board is signaling that further rate hikes will be required this year, largely to offset the economic impact of the strong labor market and contain inflation. The high – and climbing – cost of capital has already started impacting developers’ decisions on whether to move forward with construction projects.

“This is not like the last recession with respect to lack of liquidity in the marketplace. There is still money out there for good projects,” Black said. “But the rising interest rate environment is unprecedented, including the speed of the increases that have occurred over the last 12 months… Someone told me a long time ago that in real estate it is either fear or greed. We had greed for a long time in the low-interest-rate environment. It is going back to fear winning out over greed.”

“The rapid increase in the cost of capital has hit all types of funding up and down the capital stack,” Harman said. “That has given some developers pause because some projects don’t work [financially] anymore.”

The impact of those rate hikes was seen in late 2022, he said. Typically, the number of development deals and total transaction value experiences a “tremendous increase” in the fourth quarter of the year. That big increase did not happen in Q4 2022.

“This was a softening due to interest rates that peaked in the third quarter,” Harman said. “People are trying to figure out how to make capitalization work for their projects. We think this softening is going to continue into 2023.”

The funding challenge, however, is not impacting all construction projects equally.

“I have not seen a market this disjointed – both on a capital and a property level – since the 1980s,” Black said.

Although retail generally has struggled since the beginning of the pandemic, grocery-anchored retail is one of the top-performing assets currently, according to MacKenzie Capital. The hotel sector is “bifurcated” with very high-end hotels and resorts exceeding their pre-pandemic performance. The strong multi-family and industrial markets have begun to show signs of weakening. Office projects have become very difficult to finance, but developers are seeing strong markets for specialty products, including self-storage facilities, life science and laboratory spaces, and marinas.